Code

import pandas as pd

import numpy as np

from matplotlib import pyplot as plt

import seaborn as sns

plt.style.use('dark_background')

plt.style.use('seaborn')

Airbnb claims to be part of the “sharing economy” and disrupting the hotel industry. However, data shows that the majority of Airbnb listings in most cities are entire homes, many of which are rented all year round - disrupting housing and communities.

import pandas as pd

import numpy as np

from matplotlib import pyplot as plt

import seaborn as sns

plt.style.use('dark_background')

plt.style.use('seaborn')1 Year properties listing from San Francisco on Airbnb

urls = [

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-06-08/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-05-06/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-04-07/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-03-13/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-02-12/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-01-04/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2020-01-02/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-12-04/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-11-01/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-10-14/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-09-12/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-08-06/data/listings.csv',

'http://data.insideairbnb.com/united-states/ca/san-francisco/2019-07-08/data/listings.csv'

]

dfs = pd.concat([pd.read_csv(x) for x in urls],ignore_index=True)

dfs['availability'] = dfs['availability_365'] / 365

# dfs['date'] = pd.to_datetime(dfs['last_scraped'])

# dfs['dayofweek'] = dfs['date'].dt.dayofweek

# dfs['quarter'] = dfs['date'].dt.quarter

# dfs['month'] = dfs['date'].dt.month

# dfs['year'] = dfs['date'].dt.year

# dfs['dayofyear'] = dfs['date'].dt.dayofyear

# dfs['dayofmonth'] = dfs['date'].dt.day

# dfs['weekofyear'] = dfs['date'].dt.weekofyear

# time_columns = ['dayofweek','quarter','month','year','dayofyear','dayofmonth','weekofyear']

# clean price

for x in ['price','weekly_price','monthly_price','security_deposit','cleaning_fee']:

dfs[x] = dfs[x].str.replace('$','').str.replace(',','').astype(float).fillna(0)

dfs[:1]/usr/local/lib/python3.6/dist-packages/IPython/core/interactiveshell.py:2822: DtypeWarning: Columns (61,62) have mixed types.Specify dtype option on import or set low_memory=False.

if self.run_code(code, result):| id | listing_url | scrape_id | last_scraped | name | summary | space | description | experiences_offered | neighborhood_overview | notes | transit | access | interaction | house_rules | thumbnail_url | medium_url | picture_url | xl_picture_url | host_id | host_url | host_name | host_since | host_location | host_about | host_response_time | host_response_rate | host_acceptance_rate | host_is_superhost | host_thumbnail_url | host_picture_url | host_neighbourhood | host_listings_count | host_total_listings_count | host_verifications | host_has_profile_pic | host_identity_verified | street | neighbourhood | neighbourhood_cleansed | ... | minimum_nights | maximum_nights | minimum_minimum_nights | maximum_minimum_nights | minimum_maximum_nights | maximum_maximum_nights | minimum_nights_avg_ntm | maximum_nights_avg_ntm | calendar_updated | has_availability | availability_30 | availability_60 | availability_90 | availability_365 | calendar_last_scraped | number_of_reviews | number_of_reviews_ltm | first_review | last_review | review_scores_rating | review_scores_accuracy | review_scores_cleanliness | review_scores_checkin | review_scores_communication | review_scores_location | review_scores_value | requires_license | license | jurisdiction_names | instant_bookable | is_business_travel_ready | cancellation_policy | require_guest_profile_picture | require_guest_phone_verification | calculated_host_listings_count | calculated_host_listings_count_entire_homes | calculated_host_listings_count_private_rooms | calculated_host_listings_count_shared_rooms | reviews_per_month | availability | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 958 | https://www.airbnb.com/rooms/958 | 20200608144408 | 2020-06-08 | Bright, Modern Garden Unit - 1BR/1BTH | New update: the house next door is under const... | Newly remodeled, modern, and bright garden uni... | New update: the house next door is under const... | none | *Quiet cul de sac in friendly neighborhood *St... | Due to the fact that we have children and a do... | *Public Transportation is 1/2 block away. *Ce... | *Full access to patio and backyard (shared wit... | A family of 4 lives upstairs with their dog. N... | * No Pets - even visiting guests for a short t... | NaN | NaN | https://a0.muscache.com/im/pictures/b7c2a199-4... | NaN | 1169 | https://www.airbnb.com/users/show/1169 | Holly | 2008-07-31 | San Francisco, California, United States | We are a family with 2 boys born in 2009 and 2... | within an hour | 100% | 99% | t | https://a0.muscache.com/im/pictures/user/efdad... | https://a0.muscache.com/im/pictures/user/efdad... | Duboce Triangle | 1.0 | 1.0 | ['email', 'phone', 'facebook', 'reviews', 'kba'] | t | t | San Francisco, CA, United States | Duboce Triangle | Western Addition | ... | 1 | 1125 | 1 | 1 | 1125 | 1125 | 1.0 | 1125.0 | 5 weeks ago | t | 8 | 24 | 43 | 143 | 2020-06-08 | 241 | 47 | 2009-07-23 | 2020-03-28 | 97.0 | 10.0 | 10.0 | 10.0 | 10.0 | 10.0 | 10.0 | t | STR-0001256 | {"SAN FRANCISCO"} | f | f | moderate | f | f | 1 | 1 | 0 | 0 | 1.82 | 0.391781 |

1 rows × 107 columns

Latest Month

df = dfs[dfs.last_scraped == '2020-06-08'].copy()

# save a list of columns before filtering

all_columns = df.columns.tolist()

selected_columns = ['id','last_scraped','listing_url','host_id','property_type','zipcode','accommodates', 'bathrooms', 'bedrooms', 'beds', 'price', 'weekly_price','monthly_price', 'security_deposit', 'cleaning_fee','number_of_reviews','review_scores_rating','cancellation_policy','neighbourhood','availability_365','latitude','longitude']

# filter columns

df = df[selected_columns]

df[:1]| id | last_scraped | listing_url | host_id | property_type | zipcode | accommodates | bathrooms | bedrooms | beds | price | weekly_price | monthly_price | security_deposit | cleaning_fee | number_of_reviews | review_scores_rating | cancellation_policy | neighbourhood | availability_365 | latitude | longitude | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 958 | 2020-06-08 | https://www.airbnb.com/rooms/958 | 1169 | Apartment | 94117 | 3 | 1.0 | 1.0 | 2.0 | 170.0 | 1120.0 | 4200.0 | 100.0 | 100.0 | 241 | 97.0 | moderate | Duboce Triangle | 143 | 37.76931 | -122.43386 |

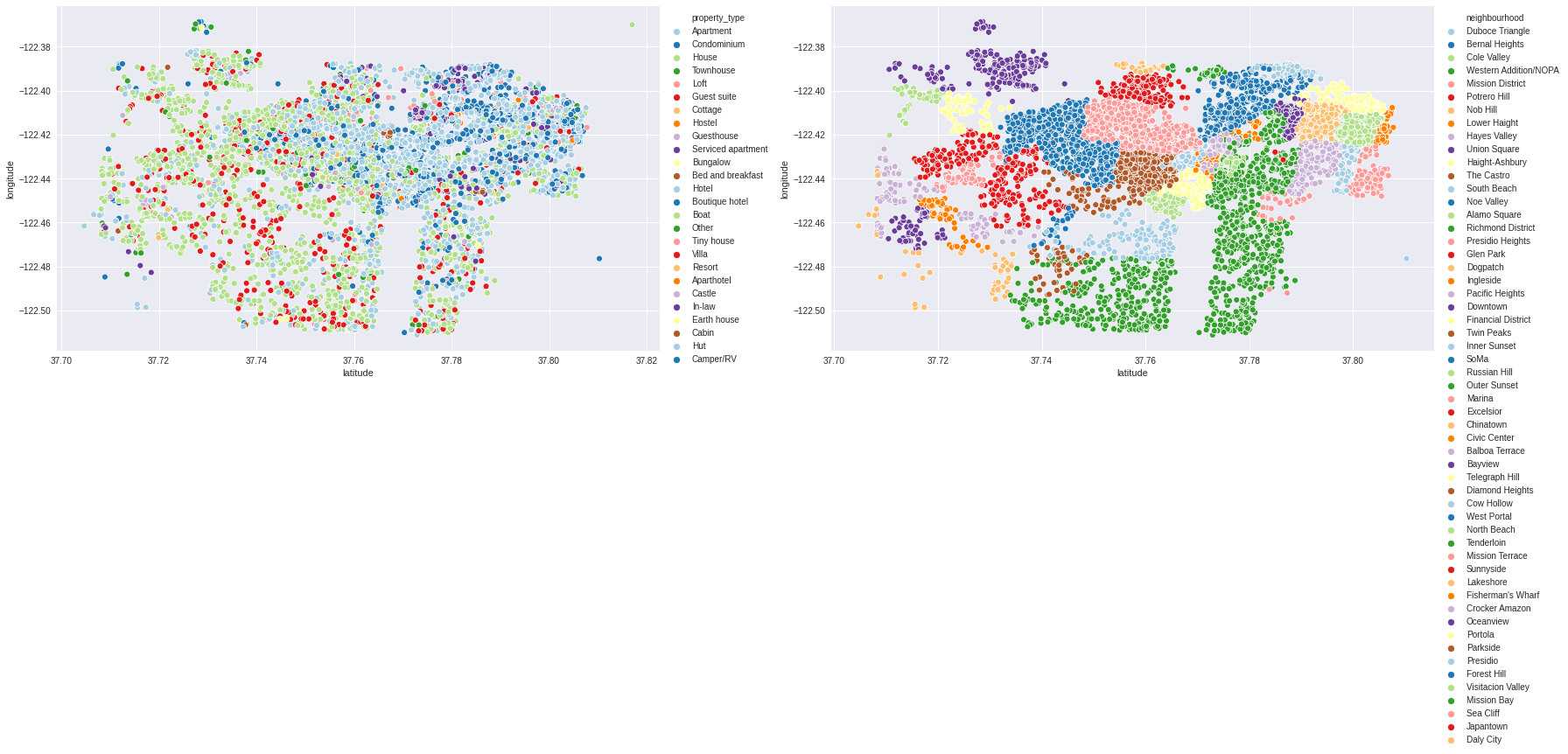

fig,ax = plt.subplots(1,2,figsize=(25,10))

sns.scatterplot(data=df,x='latitude',y='longitude',hue='property_type',palette=sns.color_palette("Paired", df.property_type.nunique()),ax=ax.ravel()[0])

sns.scatterplot(data=df,x='latitude',y='longitude',hue='neighbourhood',palette=sns.color_palette("Paired", df.neighbourhood.nunique()),ax=ax.ravel()[1])

ax.ravel()[0].legend(bbox_to_anchor=(1.0,1.0))

ax.ravel()[1].legend(bbox_to_anchor=(1.0,1.0))

plt.tight_layout()

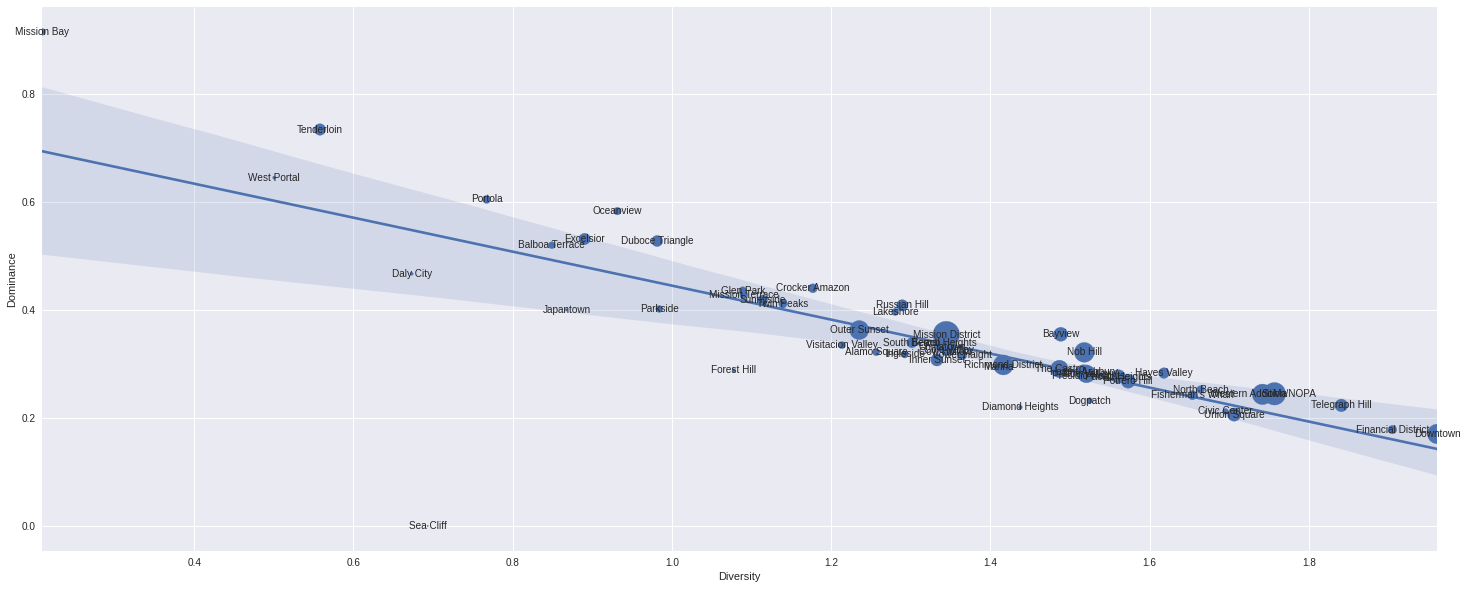

Diversity and Dominance

def shannon(series):

"""

series: pd.Series

"""

N = series.sum()

s = np.array([ (n/N) * np.log(n/N) for n in series if n != 0])

s = s[~np.isnan(s)]

return np.abs(s.sum())

def simpson(series):

"""

series: pd.Series

"""

N = series.sum()

return np.array([ ( n * (n-1) ) / ( N * (N-1) ) for n in series if n != 0]).sum()Diversity and Dominance of property types by neighbourhood

plt.figure(figsize=(25,10))

ngh = pd.crosstab(df.property_type,df.neighbourhood)

ngh_diversity = ngh.apply(shannon)

ngh_dominance = ngh.apply(simpson)

ngh_df = pd.DataFrame({

'diversity': ngh_diversity,

'dominance': ngh_dominance,

'total_number_of_properties': ngh.sum(),

'unique_property_types': df.groupby('neighbourhood').property_type.nunique()

}).reset_index()

plt.scatter(ngh_diversity,ngh_dominance,s=ngh.sum(),label='Property Type',cmap='Oranges')

sns.regplot(ngh_diversity,ngh_dominance,scatter=False)

for i,x in enumerate(ngh.columns):

plt.annotate(x,(ngh_diversity[i],ngh_dominance[i]),ha='center',va='center')

plt.xlabel('Diversity')

plt.ylabel('Dominance');/usr/local/lib/python3.6/dist-packages/ipykernel_launcher.py:21: RuntimeWarning: invalid value encountered in long_scalars

ngh_df[ngh_df.neighbourhood.isin(['Downtown','Mission District','Mission Bay'])]| neighbourhood | diversity | dominance | total_number_of_properties | unique_property_types | |

|---|---|---|---|---|---|

| 12 | Downtown | 1.961264 | 0.170480 | 382 | 12 |

| 27 | Mission Bay | 0.208982 | 0.914010 | 46 | 3 |

| 28 | Mission District | 1.344584 | 0.354231 | 705 | 11 |

Diversity and Dominance of property types by for each neighbourhood

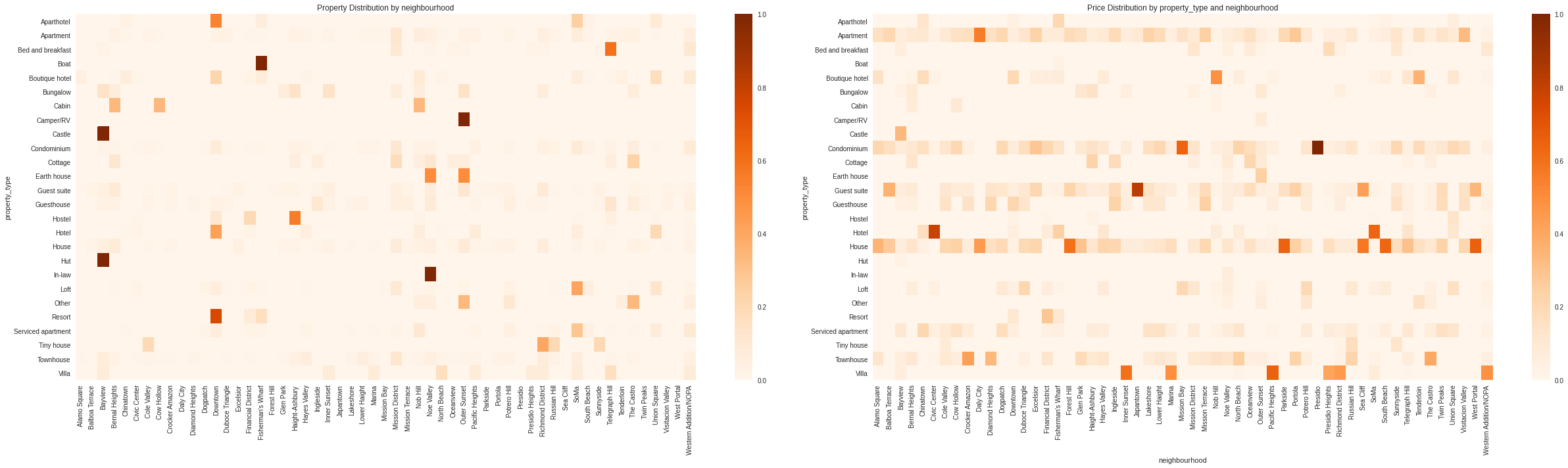

Property Distributions

fig,ax = plt.subplots(1,2,figsize=(35,10))

property_distribution = df.pivot_table(index='neighbourhood',columns='property_type',values='id',aggfunc='count',fill_value=0).T

property_distribution = property_distribution.apply(lambda x: x / x.sum(),axis=1)

sns.heatmap(property_distribution,ax=ax.ravel()[0],cmap='Oranges')

property_price = df.pivot_table(index='neighbourhood',columns='property_type',values='price',aggfunc='mean',fill_value=0)

property_price = property_price.apply(lambda x: x / x.sum(),axis=1)

sns.heatmap(property_price.T,ax=ax.ravel()[1],cmap='Oranges')

ax.ravel()[0].set_xlabel('')

# ax.ravel()[0].set_xticklabels([''])

ax.ravel()[0].set_title('Property Distribution by neighbourhood')

ax.ravel()[1].set_title('Price Distribution by property_type and neighbourhood')

plt.tight_layout()

Outliers: - Bayview: - Castle - Hut - Fisherman’s Wharf: - Boat - Nob Hill: - In-law - Outer Susnet - Camper

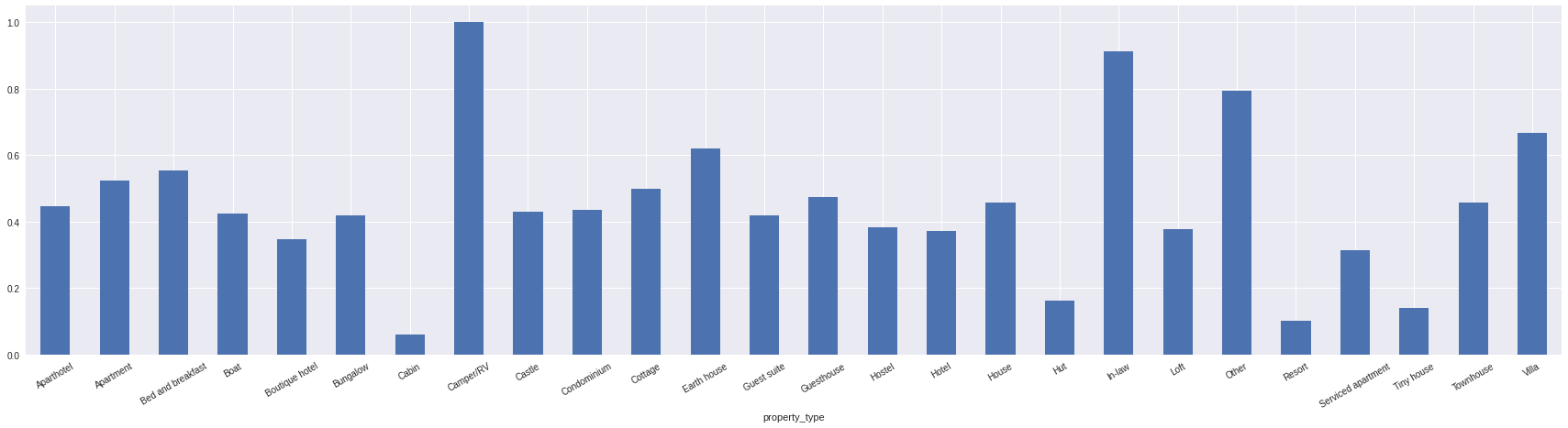

Average Yearly Availability by Property Type

(df.groupby('property_type').availability_365.mean() / 365).plot.bar(rot=30,figsize=(30,7))

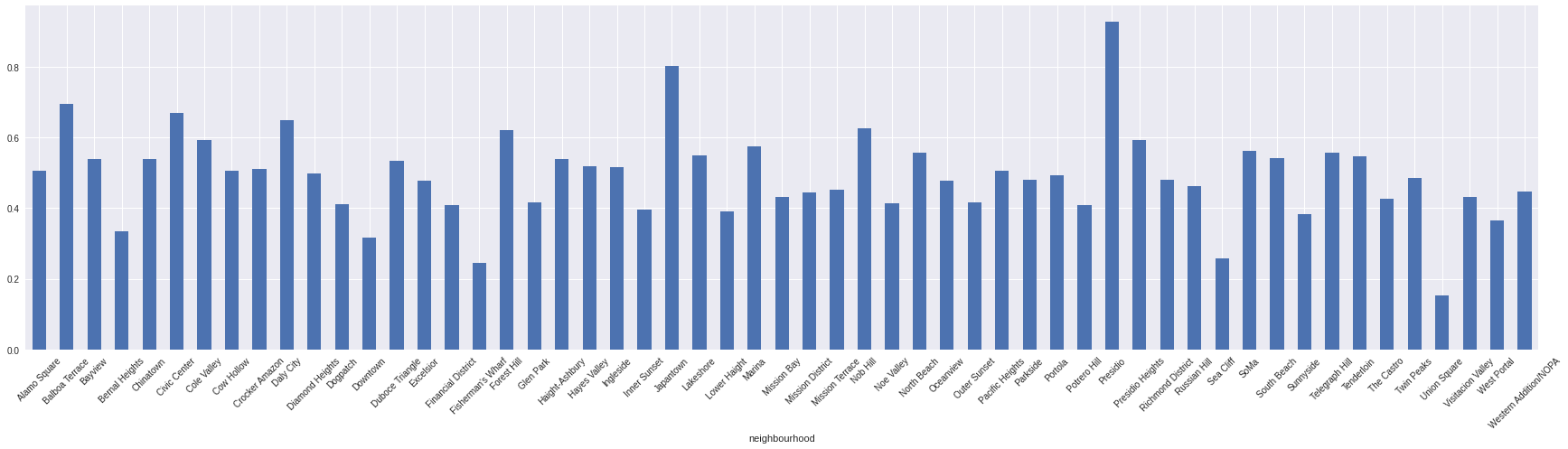

Average Yearly Availability by Neighbourhood

(df.groupby('neighbourhood').availability_365.mean() / 365).plot.bar(rot=45,figsize=(30,7))

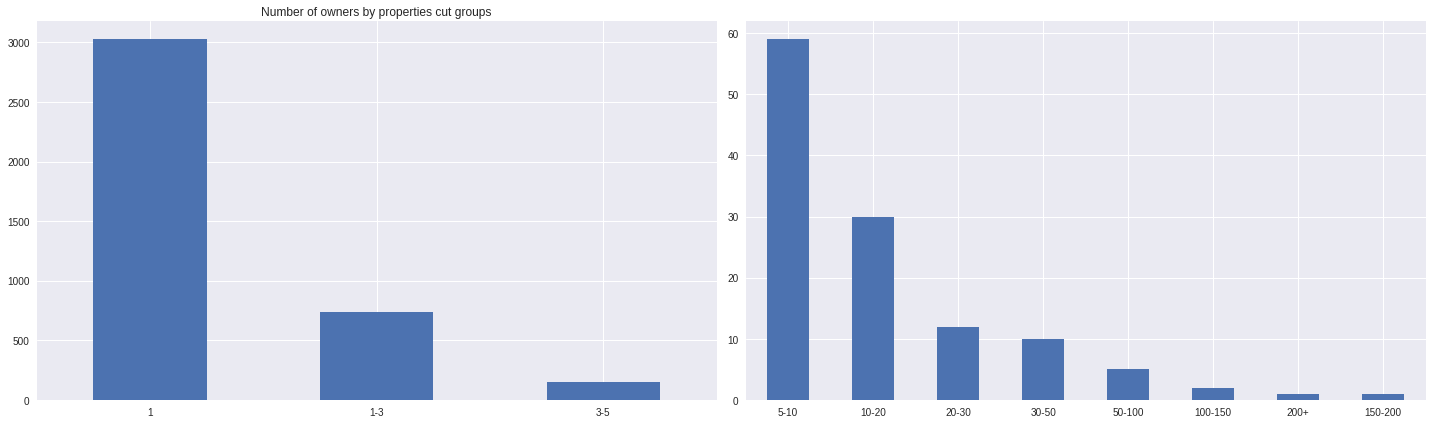

Number of hosts by range of properties

hosts = df.groupby('host_id')['id'].nunique().to_frame().reset_index().rename(columns={'id':'number_of_properties'})

bins = [0,1,3,5,10,20,30,50,100,150,200,230]

f_bins = list()

for x in range(1,len(bins)-1):

if x == 1:

f_bins.append(str(bins[1]))

else:

f_bins.append(f'{bins[x-1]}-{bins[x]}')

if x == len(bins)-2:

f_bins.append(str(bins[-2]) + '+')

hosts['group'] = pd.cut(hosts.number_of_properties,bins=bins,labels=f_bins)

fig,ax =plt.subplots(1,2,figsize=(20,6))

hosts.group.value_counts()[:3].plot.bar(rot=0,ax=ax.ravel()[0])

hosts.group.value_counts()[3:].plot.bar(rot=0,ax=ax.ravel()[1])

ax.ravel()[0].set_title('Number of owners by properties cut groups')

plt.tight_layout()

Using the mean values filtered by basic property specs

filtering_columns = ['neighbourhood','property_type','bathrooms', 'bedrooms', 'beds']

mean_prices_group = df.groupby(filtering_columns)['price'].mean().reset_index()Now let’s pick a random property and see the differences

smpl = df.sample(1).copy()

print('Sample specs')

print(smpl[filtering_columns + ['price']].T)

print('\nMean Price by same property specs')

print(smpl[filtering_columns].merge(mean_prices_group,on=filtering_columns,how='left').T)Sample specs

583

neighbourhood Lower Haight

property_type Apartment

bathrooms 2

bedrooms 2

beds 2

price 216

Mean Price by same property specs

0

neighbourhood Lower Haight

property_type Apartment

bathrooms 2

bedrooms 2

beds 2

price 357.5XGBoost

# columns for training

x_cols = ['property_type', 'accommodates', 'bathrooms', 'bedrooms',

'beds', 'weekly_price', 'monthly_price', 'security_deposit',

'cleaning_fee', 'number_of_reviews', 'review_scores_rating',

'cancellation_policy', 'neighbourhood', 'availability_365']

# copy the main dataframe

xdf = df[x_cols + ['price']].copy()

# fill missing values

xdf.loc[(xdf.neighbourhood.isnull()) & (xdf.property_type == 'Boat'),'neighbourhood'] = 'Here is a boat'

xdf = xdf.fillna(0)

#label encoding

label_encoding = dict()

to_label = ['property_type','cancellation_policy','neighbourhood']

for x in to_label:

l = xdf[x].unique()

label_encoding[x] = dict(zip( l, list(range(len(l))) ))

xdf[x] = xdf[x].map(label_encoding[x].get)

xdf[:3]| property_type | accommodates | bathrooms | bedrooms | beds | weekly_price | monthly_price | security_deposit | cleaning_fee | number_of_reviews | review_scores_rating | cancellation_policy | neighbourhood | availability_365 | price | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 3 | 1.0 | 1.0 | 2.0 | 1120.0 | 4200.0 | 100.0 | 100.0 | 241 | 97.0 | 0 | 0 | 143 | 170.0 |

| 1 | 0 | 5 | 1.0 | 2.0 | 3.0 | 1600.0 | 5500.0 | 0.0 | 100.0 | 111 | 98.0 | 1 | 1 | 0 | 235.0 |

| 2 | 0 | 2 | 4.0 | 1.0 | 1.0 | 485.0 | 1685.0 | 200.0 | 50.0 | 19 | 84.0 | 1 | 2 | 365 | 65.0 |

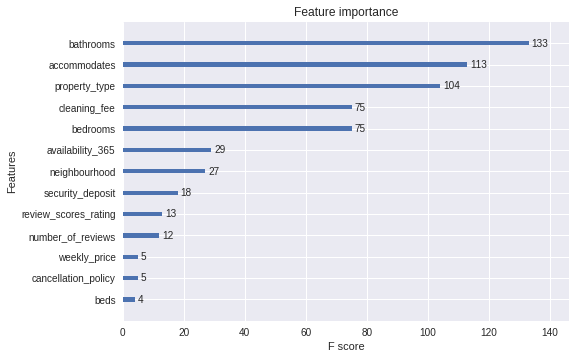

import xgboost as xgbxgr = xgb.XGBRegressor(objective='reg:gamma').fit(xdf[x_cols],xdf['price'])xgb.plot_importance(xgr)

smpl = xdf.sample(1).copy()

print('Sample specs')

print(smpl[x_cols + ['price']].T)

print(f'\nXGBoost Gamma Regressor Prediced Price {xgr.predict(smpl[x_cols])[0]}')Sample specs

7587

property_type 0.0

accommodates 2.0

bathrooms 1.0

bedrooms 1.0

beds 1.0

weekly_price 0.0

monthly_price 0.0

security_deposit 200.0

cleaning_fee 100.0

number_of_reviews 0.0

review_scores_rating 0.0

cancellation_policy 2.0

neighbourhood 43.0

availability_365 83.0

price 86.0

XGBoost Gamma Regressor Prediced Price 150.90704345703125def predict_price(df,xgr):

c_df = df.copy()

for j in to_label:

c_df[j] = c_df[j].map(label_encoding[j].get)

return xgr.predict(c_df)Estimate number of nights per year for each listing

Source: tule2236/Airbnb-Dynamic-Pricing-Optimization

As found in the Overview of the Airbnb Community in San Francisco published by Airbnb, the average length of stay per guest is 4.2 nights. We assumed each listing has 4.2 days as an average lengths of stay per booking. Since we were not able to find a clear number for the ratio of guests making a booking who leave a review for Airbnb, we assumed the review rate to be equal to 0.5, which will be used as a constant throughout the estimation. To prevent artificially high results, we also assumed the maximum occupancy rate cannot exceed 0.95, meaning even the busiest of listings will have several nights a month in which they go unrented. With these assumptions and constants, we generated the formulation of estimated occupancy rate shown below:

def estimate_nights_per_year(review_per_month,yearly_availability):

av_nights = 4.2

review_rate = 0.5

max_occupancy_rate = 0.95

bookings_per_month = review_per_month / review_rate

est_occupancy = min( (( bookings_per_month * av_nights ) / 30),max_occupancy_rate)

return est_occupancy * yearly_availabilitydf['estimated_nights_per_year'] = df.apply(lambda x : estimate_nights_per_year(x.number_of_reviews,x.availability_365),axis=1)Average estimated nights per year by neighbourhood and property type

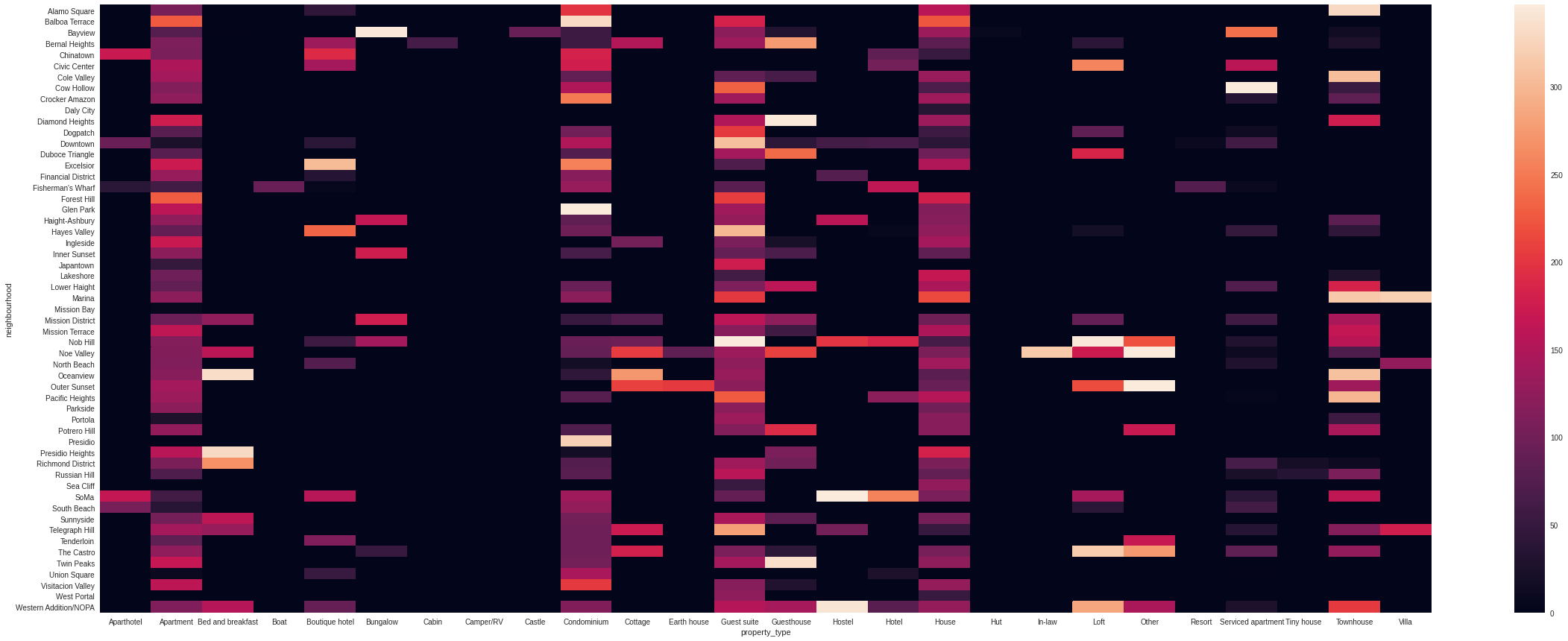

plt.figure(figsize=(40,15))

sns.heatmap(df.pivot_table(index='neighbourhood',columns='property_type',values='estimated_nights_per_year',aggfunc='mean',fill_value=0))

Since we don’t have property prices, we assume that after 20 years of activity, the property paid the price for itself.

main_columns = ['neighbourhood','property_type', 'accommodates', 'bathrooms', 'bedrooms', 'beds']

copy_df = df.copy()

# estimate number of nights per year

copy_df['estimated_nights_per_year'] = copy_df.apply(lambda x : estimate_nights_per_year(x.number_of_reviews,x.availability_365),axis=1)

# get optimized prices

copy_df['optimized_price'] = predict_price(copy_df[x_cols],xgr)

# groupb by main columns

mdf = copy_df.groupby(main_columns).agg({

'availability_365': 'mean',

'price': ['mean','std'],

'number_of_reviews':'mean',

'estimated_nights_per_year':'mean',

'optimized_price': ['mean','std']

}).reset_index().dropna()

# join multi-indexes together

mdf.columns = [ '_'.join(x) if x[1] != '' else x[0] for x in mdf.columns ]

# calculate return per year

mdf['estimated_return_per_year'] = mdf['price_mean'] * mdf['estimated_nights_per_year_mean']

# calculate optimized return per year

mdf['estimated_optimized_return_per_year'] = mdf['optimized_price_mean'] * mdf['estimated_nights_per_year_mean']

# generate property price

mdf['estimated_property_price'] = mdf['price_mean'] * (365 * 20)

# format property price

mdf['estimated_property_price_M'] = (mdf['estimated_property_price'] / 1e6).map(lambda x: f'$ {x:.4f}')

mdf[:3]| neighbourhood | property_type | accommodates | bathrooms | bedrooms | beds | availability_365_mean | price_mean | price_std | number_of_reviews_mean | estimated_nights_per_year_mean | optimized_price_mean | optimized_price_std | estimated_return_per_year | estimated_optimized_return_per_year | estimated_property_price | estimated_property_price_M | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | Alamo Square | Apartment | 1 | 3.0 | 1.0 | 1.0 | 364.25 | 48.0 | 6.000000 | 3.25 | 86.6875 | 57.929253 | 4.668282 | 4161.00 | 5021.742087 | 350400.0 | $ 0.3504 |

| 3 | Alamo Square | Apartment | 2 | 1.0 | 1.0 | 1.0 | 317.50 | 152.0 | 32.526912 | 26.50 | 128.2500 | 154.892731 | 17.912474 | 19494.00 | 19864.992714 | 1109600.0 | $ 1.1096 |

| 6 | Alamo Square | Apartment | 4 | 1.0 | 1.0 | 2.0 | 159.50 | 150.0 | 98.994949 | 9.50 | 151.5250 | 166.732971 | 5.983315 | 22728.75 | 25264.213460 | 1095000.0 | $ 1.0950 |

Portfolios

# 10M $ to invest

investment = 1e7

mc_portfolios = list()

pmax=100

for p in range(pmax):

print(f'{p}/{pmax}',end='\r')

#while we have money, pick up random properties for portfolio

local_df = mdf.copy()

current_money = investment

picked_properties = list()

stop_flag = False

while stop_flag != True:

# pick up random property

ch = local_df.sample(1).copy()

# if we have money to buy it and we haven't already bought it then let's do it

if ch.estimated_property_price.values[0] < current_money and ch.index.values[0] not in picked_properties:

# add property index to current portfolio list of properties

picked_properties.append(ch.index.values[0])

# pay the property price

current_money -= ch.estimated_property_price.values[0]

# slice the current dataframe to get just affordable properties

local_df = local_df[local_df.estimated_property_price < current_money]

# if we dont't have enough money to buy the event the cheapest property or we run out of properties then it's the time to stop

if current_money < local_df.estimated_property_price.min() or len(local_df) < 1:

stop_flag = True

tmp_portfolio = mdf[mdf.index.isin(picked_properties)].copy()

tmp_portfolio['mdf_id'] = picked_properties

tmp_portfolio['p'] = p

mc_portfolios.append(tmp_portfolio)

mc_portfolios = pd.concat(mc_portfolios).reset_index(drop=True)

mc_portfolios[:2]| neighbourhood | property_type | accommodates | bathrooms | bedrooms | beds | availability_365_mean | price_mean | price_std | number_of_reviews_mean | estimated_nights_per_year_mean | optimized_price_mean | optimized_price_std | estimated_return_per_year | estimated_optimized_return_per_year | estimated_property_price | estimated_property_price_M | mdf_id | p | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Bernal Heights | Condominium | 4 | 1.5 | 2.0 | 2.0 | 17.5 | 244.50 | 106.773124 | 50.50 | 16.625 | 245.411896 | 0.479673 | 4064.8125 | 4079.972767 | 1784850.0 | $ 1.7849 | 2726 | 0 |

| 1 | Chinatown | Apartment | 1 | 1.5 | 1.0 | 1.0 | 349.5 | 65.25 | 13.817260 | 2.75 | 240.510 | 92.636261 | 2.107101 | 15693.2775 | 22279.947130 | 476325.0 | $ 0.4763 | 187 | 0 |

portfolio_results = mc_portfolios.groupby('p').agg({

'estimated_return_per_year': 'sum',

'estimated_property_price': 'sum',

'estimated_optimized_return_per_year': 'sum',

'mdf_id': 'count',

}).reset_index()

portfolio_results['estimated_property_price_M'] = (portfolio_results['estimated_property_price'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['estimated_return_per_year_M'] = (portfolio_results['estimated_return_per_year'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['estimated_optimized_return_per_year_M'] = (portfolio_results['estimated_optimized_return_per_year'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['time_to_return'] = portfolio_results['estimated_property_price'] / portfolio_results['estimated_return_per_year']

portfolio_results['time_to_return_optimized'] = portfolio_results['estimated_property_price'] / portfolio_results['estimated_optimized_return_per_year']

portfolio_results['profit'] = (portfolio_results['time_to_return'] * portfolio_results['estimated_optimized_return_per_year']) - (portfolio_results['time_to_return'] * portfolio_results['estimated_return_per_year'])

portfolio_results['profit_of_investment'] = portfolio_results['profit'] / portfolio_results['estimated_property_price']

portfolio_results['profit_M'] = (portfolio_results['profit'] / 1e6).map(lambda x: f'$ {x:.4f}')Portfolios with minimal return time

portfolio_results.sort_values(by='time_to_return_optimized',ascending=True)[:3]| p | estimated_return_per_year | estimated_property_price | estimated_optimized_return_per_year | mdf_id | estimated_property_price_M | estimated_return_per_year_M | estimated_optimized_return_per_year_M | time_to_return | time_to_return_optimized | profit | profit_of_investment | profit_M | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 39 | 39 | 222350.258407 | 9.966736e+06 | 339534.248750 | 13 | $ 9.9667 | $ 0.2224 | $ 0.3395 | 44.824486 | 29.354140 | 5.252712e+06 | 0.527024 | $ 5.2527 |

| 66 | 66 | 219921.792321 | 9.931917e+06 | 309218.686489 | 7 | $ 9.9319 | $ 0.2199 | $ 0.3092 | 45.161129 | 32.119393 | 4.032749e+06 | 0.406039 | $ 4.0327 |

| 35 | 35 | 189177.550040 | 9.990919e+06 | 296431.938938 | 8 | $ 9.9909 | $ 0.1892 | $ 0.2964 | 52.812393 | 33.703922 | 5.664361e+06 | 0.566951 | $ 5.6644 |

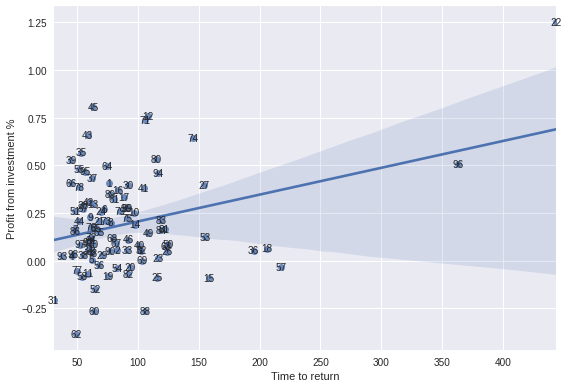

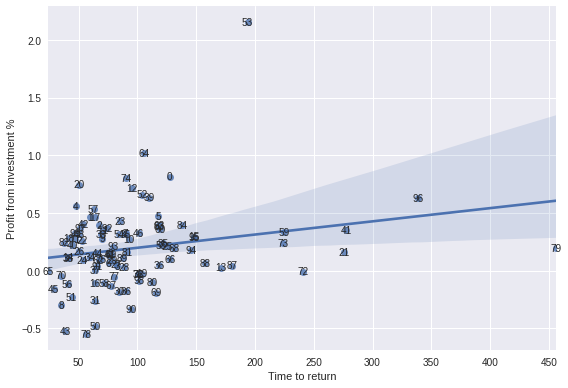

Time is money

Profit vs Time to return

sns.regplot(portfolio_results['time_to_return'],portfolio_results['profit_of_investment'])

for x in portfolio_results.itertuples():

plt.annotate(x.p,(x.time_to_return, x.profit_of_investment),ha='center',va='center')

plt.xlabel('Time to return')

plt.ylabel('Profit from investment %')

plt.tight_layout()

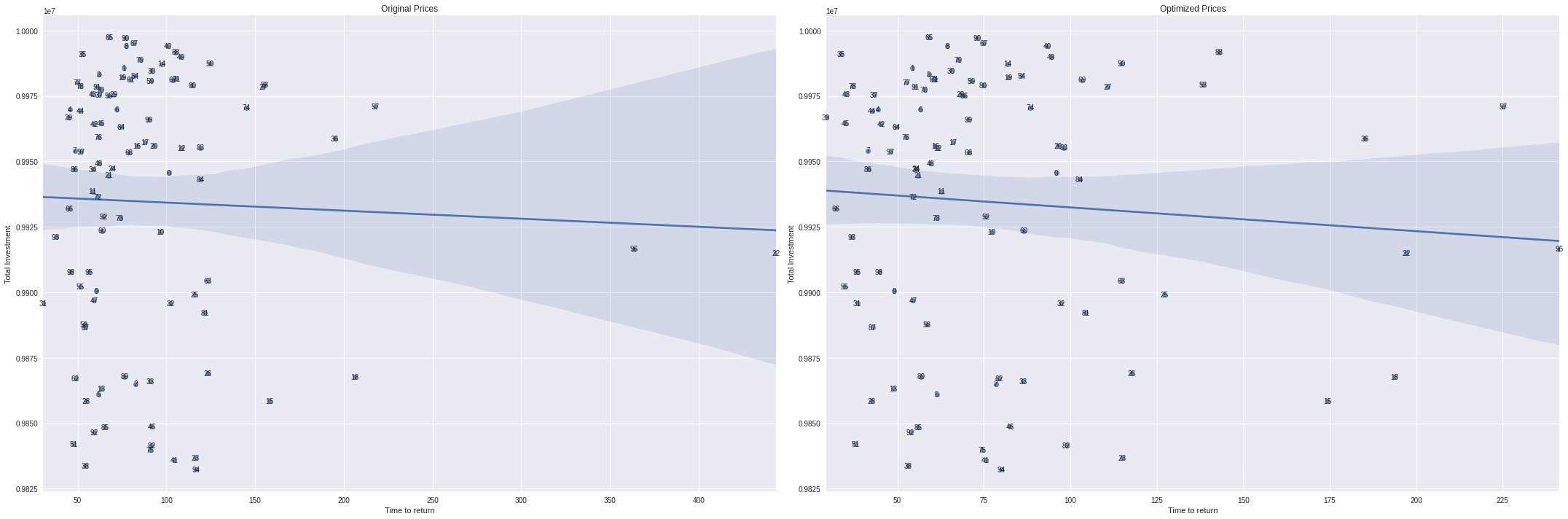

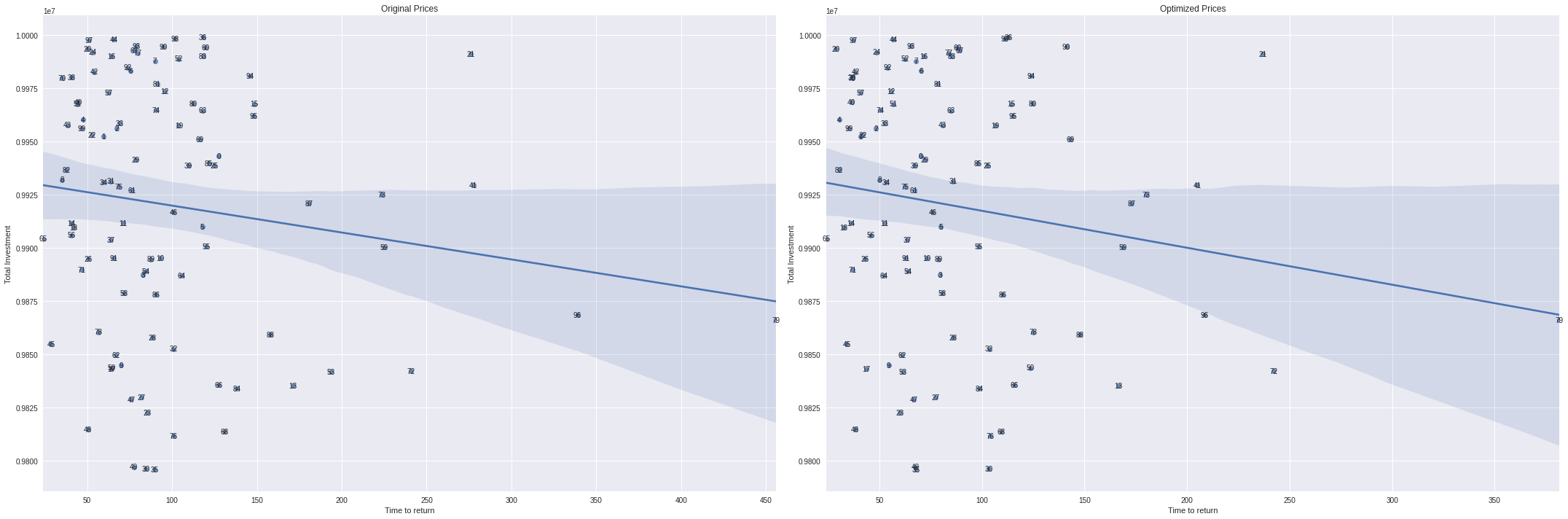

Portfolios by time and profit

fig,ax = plt.subplots(1,2,figsize=(30,10))

sns.regplot(portfolio_results['time_to_return'],portfolio_results['estimated_property_price'],ax=ax[0])

sns.regplot(portfolio_results['time_to_return_optimized'],portfolio_results['estimated_property_price'],ax=ax[1])

for x in portfolio_results.itertuples():

ax[0].annotate(x.p,(x.time_to_return, x.estimated_property_price),ha='center',va='center')

ax[1].annotate(x.p,(x.time_to_return_optimized, x.estimated_property_price),ha='center',va='center')

ax[0].set_xlabel('Time to return')

ax[0].set_ylabel('Total Investment')

ax[0].set_title('Original Prices')

ax[1].set_xlabel('Time to return')

ax[1].set_ylabel('Total Investment')

ax[1].set_title('Optimized Prices')

plt.tight_layout()

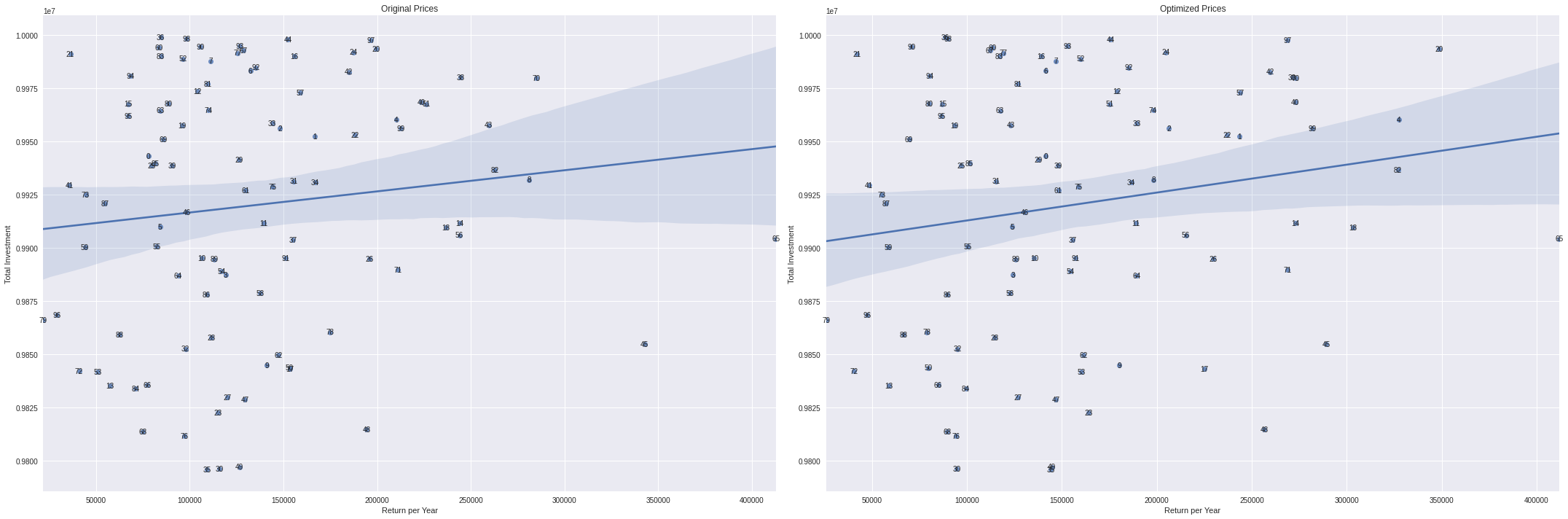

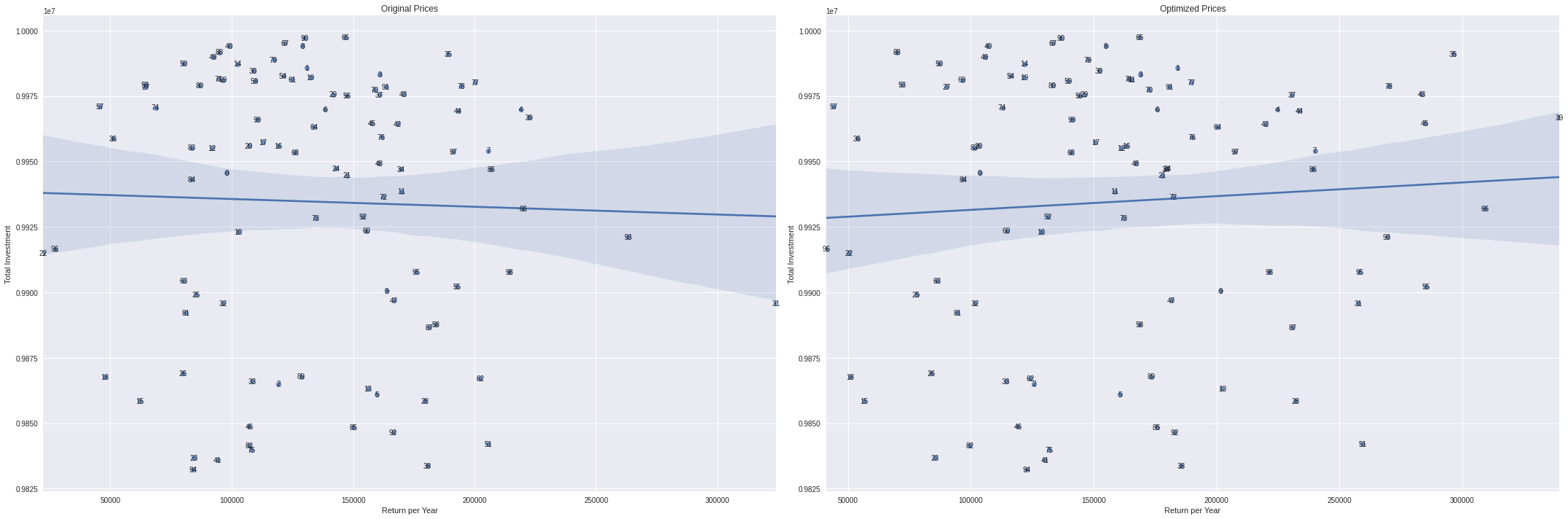

Portfolios by yearly return and total investment

fig,ax = plt.subplots(1,2,figsize=(30,10))

sns.regplot(portfolio_results['estimated_return_per_year'],portfolio_results['estimated_property_price'],ax=ax[0])

sns.regplot(portfolio_results['estimated_optimized_return_per_year'],portfolio_results['estimated_property_price'],ax=ax[1])

for x in portfolio_results.itertuples():

ax[0].annotate(x.p,(x.estimated_return_per_year, x.estimated_property_price),ha='center',va='center')

ax[1].annotate(x.p,(x.estimated_optimized_return_per_year, x.estimated_property_price),ha='center',va='center')

ax[0].set_xlabel('Return per Year')

ax[0].set_ylabel('Total Investment')

ax[0].set_title('Original Prices')

ax[1].set_xlabel('Return per Year')

ax[1].set_ylabel('Total Investment')

ax[1].set_title('Optimized Prices')

plt.tight_layout()

grp = dfs.groupby('id').agg({

'host_id':'first',

'neighbourhood':'first',

'property_type':'first',

'accommodates': 'mean',

'bathrooms':'mean',

'bedrooms': 'mean',

'beds':'mean',

'price':'mean',

'number_of_reviews':'mean',

'availability_365':'mean',

'review_scores_rating': 'mean',

'monthly_price': 'mean',

'security_deposit': 'mean',

'cleaning_fee': 'mean',

'cancellation_policy': 'first',

'weekly_price': 'mean'

}).reset_index()

grp[:3]| id | host_id | neighbourhood | property_type | accommodates | bathrooms | bedrooms | beds | price | number_of_reviews | availability_365 | review_scores_rating | monthly_price | security_deposit | cleaning_fee | cancellation_policy | weekly_price | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 958 | 1169 | Duboce Triangle | Apartment | 3.0 | 1.0 | 1.0 | 2.0 | 170.0 | 224.769231 | 90.153846 | 97.000 | 4200.0 | 100.0 | 100.0 | moderate | 1120.0 |

| 1 | 3850 | 4921 | Inner Sunset | House | 2.0 | 1.0 | 1.0 | 1.0 | 99.0 | 159.250000 | 66.250000 | 94.375 | 0.0 | 0.0 | 10.0 | strict_14_with_grace_period | 0.0 |

| 2 | 5858 | 8904 | Bernal Heights | Apartment | 5.0 | 1.0 | 2.0 | 3.0 | 235.0 | 111.000000 | 0.076923 | 98.000 | 5500.0 | 0.0 | 100.0 | strict_14_with_grace_period | 1600.0 |

location group

main_columns = ['neighbourhood','property_type', 'accommodates', 'bathrooms', 'bedrooms', 'beds']

copy_df = grp.copy()

copy_df['estimated_nights_per_year'] = copy_df.apply(lambda x : estimate_nights_per_year(x.number_of_reviews,x.availability_365),axis=1)

copy_df['optimized_price'] = predict_price(copy_df[x_cols],xgr)

mdf = copy_df.groupby(main_columns).agg({

'availability_365': 'mean',

'price': ['mean','std'],

'number_of_reviews':'mean',

'estimated_nights_per_year':['mean','std'],

'optimized_price': ['mean','std']

}).reset_index().dropna()

mdf.columns = [ '_'.join(x) if x[1] != '' else x[0] for x in mdf.columns ]

returns = list()

optimized_returns = list()

for x in mdf.itertuples():

# generate random number of nights using the mean and std of estimated nights per year

random_nights = np.abs(np.random.normal(loc=x.estimated_nights_per_year_mean,scale=x.estimated_nights_per_year_std))

# generate random prices with the size of the random nights

random_prices = np.random.normal(loc=x.price_mean,scale=x.price_std,size=int(random_nights))

# add the yearly return to our list

returns.append(random_prices.sum())

# for the same number of random nights, calculate the optimized yearly return

random_optim_prices = np.random.normal(loc=x.optimized_price_mean,scale=x.optimized_price_std,size=int(random_nights))

optimized_returns.append(random_optim_prices.sum())

mdf['estimated_return_per_year'] = returns

mdf['estimated_optimized_return_per_year'] = optimized_returns

mdf['estimated_property_price'] = mdf['price_mean'] * (365 * 20)

mdf['estimated_property_price_M'] = (mdf['estimated_property_price'] / 1e6).map(lambda x: f'$ {x:.4f}')

mdf[:3]| neighbourhood | property_type | accommodates | bathrooms | bedrooms | beds | availability_365_mean | price_mean | price_std | number_of_reviews_mean | estimated_nights_per_year_mean | estimated_nights_per_year_std | optimized_price_mean | optimized_price_std | estimated_return_per_year | estimated_optimized_return_per_year | estimated_property_price | estimated_property_price_M | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | Alamo Square | Apartment | 1.0 | 3.0 | 1.0 | 1.0 | 348.685897 | 47.000000 | 4.898979 | 2.191026 | 75.109436 | 127.222971 | 60.804733 | 4.177582 | 11603.875568 | 14897.434087 | 3.431000e+05 | $ 0.3431 |

| 3 | Alamo Square | Apartment | 2.0 | 1.0 | 1.0 | 1.0 | 199.173789 | 135.333333 | 36.909800 | 13.307692 | 72.541026 | 125.644742 | 156.995514 | 13.179280 | 21458.311016 | 25192.637399 | 9.879333e+05 | $ 0.9879 |

| 9 | Alamo Square | Apartment | 4.0 | 1.0 | 1.0 | 2.0 | 159.062500 | 156.250000 | 90.156115 | 9.375000 | 151.109375 | 213.700928 | 166.732971 | 5.983315 | 2647.978633 | 2840.720439 | 1.140625e+06 | $ 1.1406 |

# 10M $ to invest

investment = 1e7

mc_portfolios = list()

pmax=100

for p in range(pmax):

print(f'{p}/{pmax}',end='\r')

#while we have money, pick up random properties for portfolio

local_df = mdf.copy()

current_money = investment

picked_properties = list()

stop_flag = False

while stop_flag != True:

# pick up random property

ch = local_df.sample(1).copy()

# if we have money to buy it and we haven't already bought it then let's do it

if ch.estimated_property_price.values[0] < current_money and ch.index.values[0] not in picked_properties:

# add property index to current portfolio list of properties

picked_properties.append(ch.index.values[0])

# pay the property price

current_money -= ch.estimated_property_price.values[0]

# slice the current dataframe to get just affordable properties

local_df = local_df[local_df.estimated_property_price < current_money]

# if we dont't have enough money to buy even the cheapest property or we run out of properties then it's the time to stop

if current_money < local_df.estimated_property_price.min() or len(local_df) < 1:

stop_flag = True

tmp_portfolio = mdf[mdf.index.isin(picked_properties)].copy()

tmp_portfolio['mdf_id'] = picked_properties

tmp_portfolio['p'] = p

mc_portfolios.append(tmp_portfolio)

mc_portfolios = pd.concat(mc_portfolios).reset_index(drop=True)

mc_portfolios[:2]| neighbourhood | property_type | accommodates | bathrooms | bedrooms | beds | availability_365_mean | price_mean | price_std | number_of_reviews_mean | estimated_nights_per_year_mean | estimated_nights_per_year_std | optimized_price_mean | optimized_price_std | estimated_return_per_year | estimated_optimized_return_per_year | estimated_property_price | estimated_property_price_M | mdf_id | p | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Bayview | House | 2.0 | 2.0 | 1.0 | 1.0 | 235.420994 | 84.28125 | 47.190994 | 3.540064 | 161.430898 | 111.271046 | 139.239120 | 19.414377 | 20207.811891 | 35149.639528 | 615253.125 | $ 0.6153 | 2932 | 0 |

| 1 | Bayview | House | 8.0 | 3.0 | 4.0 | 4.0 | 25.307692 | 262.50000 | 53.033009 | 14.300000 | 24.042308 | 32.657455 | 549.040161 | 8.945264 | 10060.290051 | 21961.733177 | 1916250.000 | $ 1.9163 | 213 | 0 |

portfolio_results = mc_portfolios.groupby('p').agg({

'estimated_return_per_year': 'sum',

'estimated_property_price': 'sum',

'estimated_optimized_return_per_year': 'sum',

'mdf_id': 'count',

}).reset_index()

portfolio_results['estimated_property_price_M'] = (portfolio_results['estimated_property_price'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['estimated_return_per_year_M'] = (portfolio_results['estimated_return_per_year'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['estimated_optimized_return_per_year_M'] = (portfolio_results['estimated_optimized_return_per_year'] / 1e6).map(lambda x: f'$ {x:.4f}')

portfolio_results['time_to_return'] = portfolio_results['estimated_property_price'] / portfolio_results['estimated_return_per_year']

portfolio_results['time_to_return_optimized'] = portfolio_results['estimated_property_price'] / portfolio_results['estimated_optimized_return_per_year']

portfolio_results['profit'] = (portfolio_results['time_to_return'] * portfolio_results['estimated_optimized_return_per_year']) - (portfolio_results['time_to_return'] * portfolio_results['estimated_return_per_year'])

portfolio_results['profit_of_investment'] = portfolio_results['profit'] / portfolio_results['estimated_property_price']

portfolio_results['profit_M'] = (portfolio_results['profit'] / 1e6).map(lambda x: f'$ {x:.4f}')Portfolios with minimal return time

portfolio_results.sort_values(by='time_to_return_optimized',ascending=True)[:3]| p | estimated_return_per_year | estimated_property_price | estimated_optimized_return_per_year | mdf_id | estimated_property_price_M | estimated_return_per_year_M | estimated_optimized_return_per_year_M | time_to_return | time_to_return_optimized | profit | profit_of_investment | profit_M | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 65 | 65 | 413167.932968 | 9.904386e+06 | 411843.015193 | 7 | $ 9.9044 | $ 0.4132 | $ 0.4118 | 23.971816 | 24.048934 | -3.176069e+04 | -0.003207 | $ -0.0318 |

| 20 | 20 | 199503.023973 | 9.993643e+06 | 348561.432544 | 10 | $ 9.9936 | $ 0.1995 | $ 0.3486 | 50.092689 | 28.671109 | 7.466737e+06 | 0.747149 | $ 7.4667 |

| 82 | 82 | 262761.351114 | 9.936821e+06 | 326939.359423 | 10 | $ 9.9368 | $ 0.2628 | $ 0.3269 | 37.816904 | 30.393468 | 2.427014e+06 | 0.244244 | $ 2.4270 |

sns.regplot(portfolio_results['time_to_return'],portfolio_results['profit_of_investment'])

for x in portfolio_results.itertuples():

plt.annotate(x.p,(x.time_to_return, x.profit_of_investment),ha='center',va='center')

plt.xlabel('Time to return')

plt.ylabel('Profit from investment %')

plt.tight_layout()

Portfolios by time to return and total investment

fig,ax = plt.subplots(1,2,figsize=(30,10))

sns.regplot(portfolio_results['time_to_return'],portfolio_results['estimated_property_price'],ax=ax[0])

sns.regplot(portfolio_results['time_to_return_optimized'],portfolio_results['estimated_property_price'],ax=ax[1])

for x in portfolio_results.itertuples():

ax[0].annotate(x.p,(x.time_to_return, x.estimated_property_price),ha='center',va='center')

ax[1].annotate(x.p,(x.time_to_return_optimized, x.estimated_property_price),ha='center',va='center')

ax[0].set_xlabel('Time to return')

ax[0].set_ylabel('Total Investment')

ax[0].set_title('Original Prices')

ax[1].set_xlabel('Time to return')

ax[1].set_ylabel('Total Investment')

ax[1].set_title('Optimized Prices')

plt.tight_layout()

Huge return time

Most probaby because there are some properties with just few days per year availability

portfolio_results.sort_values(by='time_to_return_optimized',ascending=False)[:3]| p | estimated_return_per_year | estimated_property_price | estimated_optimized_return_per_year | mdf_id | estimated_property_price_M | estimated_return_per_year_M | estimated_optimized_return_per_year_M | time_to_return | time_to_return_optimized | profit | profit_of_investment | profit_M | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 79 | 79 | 21630.442249 | 9.866244e+06 | 25863.355133 | 6 | $ 9.8662 | $ 0.0216 | $ 0.0259 | 456.127712 | 381.475802 | 1.930749e+06 | 0.195692 | $ 1.9307 |

| 72 | 72 | 40881.997953 | 9.842167e+06 | 40613.729134 | 8 | $ 9.8422 | $ 0.0409 | $ 0.0406 | 240.745749 | 242.335965 | -6.458458e+04 | -0.006562 | $ -0.0646 |

| 21 | 21 | 36208.247995 | 9.991117e+06 | 42171.958689 | 7 | $ 9.9911 | $ 0.0362 | $ 0.0422 | 275.934828 | 236.913745 | 1.645595e+06 | 0.164706 | $ 1.6456 |

Portfolios by yearly return and total investment

fig,ax = plt.subplots(1,2,figsize=(30,10))

sns.regplot(portfolio_results['estimated_return_per_year'],portfolio_results['estimated_property_price'],ax=ax[0])

sns.regplot(portfolio_results['estimated_optimized_return_per_year'],portfolio_results['estimated_property_price'],ax=ax[1])

for x in portfolio_results.itertuples():

ax[0].annotate(x.p,(x.estimated_return_per_year, x.estimated_property_price),ha='center',va='center')

ax[1].annotate(x.p,(x.estimated_optimized_return_per_year, x.estimated_property_price),ha='center',va='center')

ax[0].set_xlabel('Return per Year')

ax[0].set_ylabel('Total Investment')

ax[0].set_title('Original Prices')

ax[1].set_xlabel('Return per Year')

ax[1].set_ylabel('Total Investment')

ax[1].set_title('Optimized Prices')

plt.tight_layout()